Financial fraud is among the leading causes of profit loss to businesses that rely on money transactions. Whether it’s a banking app or a retail company, compromised security poses an enormous threat to a business’s operations. In addition to financial damages, fraud also contributes to decreased customer loyalty and potential legal issues, particularly when it infiltrates fintech apps that are expected to always be at peak reliability.

To guard against fraud, banks and financial institutions in 2021 employ machine learning. ML-based fraud detection is an effective and cost-saving solution that can help you recognize and deflect hacking attempts before they can do any damage.

Besides, machine learning is a rapidly growing tool—a part of the global fraud detection and prevention market that’s expected to hit $40.8 billion by 2026—and it can be applied across all your services and platforms.

Read on to learn more about how machine learning for fraud detection helps the finance and banking industry players protect their internal processes and deliver secure services to customers.

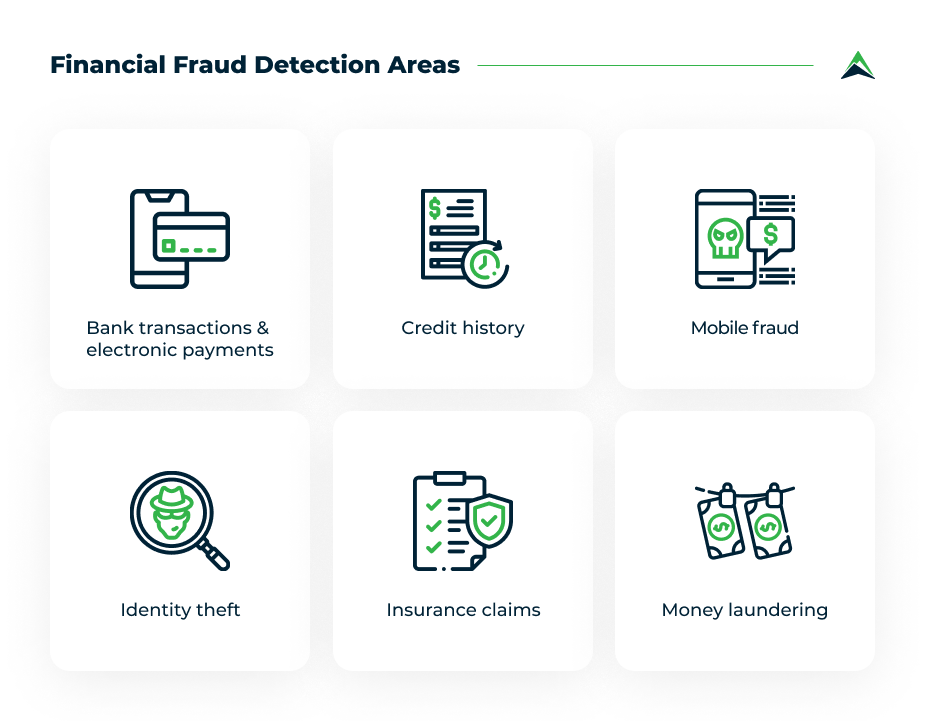

The main areas for financial fraud detection

Before we dive into the intricacies of machine learning, let’s take a look at what financial fraud is. Typically, the intention of any malicious activity is to obtain money through intercepting, modifying, or encrypting financial data.

Here are some of the most pervasive types of fraud and, consequently, areas where financial fraud detection software can greatly assist businesses.

Bank transactions and electronic payments

Bank fraud detection sits at the top of the priorities list, considering online and offline transaction scams are the most widespread kind of financial fraud.

Here are several examples of offline fraud you may encounter:

- Ghost invoices: fake invoices from companies that don’t exist or business representatives whose identity a fraudster assumes. Machine learning algorithms for fraud detection can distinguish legitimate invoices from forged ones.

- Stolen cards: even if a client is physically present at the bank, it’s necessary to verify the person is the rightful holder of the card. That’s why using machine learning to detect credit card fraud is crucial even in offline settings.

An area even larger and relatively harder to defend is online payments. Digital payment systems are everywhere, and businesses that use them, as well as fintech companies that develop them, need to be mindful of numerous scenarios for electronic financial transaction card fraud.

The common schemes include

- Phishing: an attempt to steal a person’s passwords and other personal details by posing as a legitimate organization. An example of phishing is when a user is prompted to input their card details on a site that looks genuine but is, in fact, fake and malicious.

- Fake online marketplaces: these attract customers through fake reviews and deliver counterfeit products or fail to deliver the ordered items at all. By performing a sentiment analysis, an ML system can uncover such merchants and protect customers.

- Identity theft: stealing a client’s personal data to gain access to their accounts and funds. Later in the article we will cover why exactly knowing how to prevent financial fraud in identity theft scenarios is crucial.

Credit history

Financial fraud and machine learning also come together in credit history falsifications. Banks need to detect instances of fraudulent debt reduction and automate the process of credit history checking to streamline their operations.

In the first case, fraud detection machine learning algorithms help quickly and accurately identify which actions are authentic. If a client tries to cheat the system, an ML model can alert the bank and take measures to negate the activity.

ML can also be used to process each person’s current income, transactions, credit standings with other financial institutions, and personal information (including open-source data from social media) to automate the evaluation process for granting credit. This way, companies can improve their decisions while reducing the amount and scope of the manual work required.

Mobile fraud

Integrating machine learning in anti-fraud systems is particularly crucial in 2021 when payment methods extend beyond physical cards and into the realm of mobile phones.

Smartphones now come with NFC chips, enabling users to pay for products just with their phones. This presents additional risks to cybersecurity. Machine learning is an effective solution to detect abnormal activities for each user, minimizing the damages from mobile fraud.

Identity theft

An identity is a composition of data points that allow fintech companies and banks to distinguish between their clients. This data includes a person’s name, email address, passwords and login credentials, passport details, credit history, physical address, phone number, and other extremely sensitive parameters.

All of these can be stolen in financial fraud cases to assume the identity of another person and use their bank account to make (potentially illegal) purchases or, alternatively, register new cards, assets, and accounts in the victim’s name.

Financial identity fraud typically manifests as account takeover or synthetic theft.

- Account takeover occurs when the stolen data is used to gain access to a person’s current accounts.

- Synthetic theft means creating new personalities by combining the stolen data and forged details.

Machine learning enhances security by checking clients’ passports, driver’s licenses, PAN cards, and other documents and information for validity, inferring conclusions by looking not at a single document but the overall picture. Besides, ML is useful for fighting fake IDs by enabling biometric scanning and face recognition.

Insurance claims

Insurance scams are among the most frequent financial fraud examples. They typically include fake claims of property or car damage, as well as unemployment claims. To reduce the possibility of fraud, insurance companies spend extensive amounts of time and resources to validate each separate claim—in addition to being expensive, this process is also not hacker-proof.

In the insurance industry, fraud is generally conducted through fake claims, which are completely untrue, and duplicate or exaggerated claims, which strive to receive additional compensation for an accident that the insurance company has already covered.

Due to its superior pattern recognition capabilities and substantial processing capacity, ML in fraud detection systems helps resolve insurance claims with greater accuracy.

Money laundering

Anti-money laundering software is another demonstration of how machine learning can be used in fraud detection. Most current bank systems apply approaches that use explicitly written instructions to detect money laundering.

In addition to being slow and hard to update, these tools result in high volumes of false-positive results, damaging both the accuracy of examinations and the robustness of banks’ operations.

Machine learning and AI aid in anti-money laundering attempts by applying statistical analysis to validate customer information and semantic analysis to detect duplicate or redundant data. ML also recognizes patterns that trigger false-positive results, thus greatly reducing the number of invalid alerts.

Why use machine learning in fintech?

Before machine learning became sophisticated enough, companies had been bound to use rule-based systems for financial fraud prevention. The rule-based approach relies on explicitly written instructions. It identifies digital fraudulent activities by comparing them against the rules written by cybersecurity specialists and detecting abnormalities.

To validate each transaction, the rule-based approach typically applies a couple hundred tests. If any of them fail, the transaction may require additional verification to go through.

Although such a system can safeguard against the most common attacks, it is incredibly difficult to update and adjust, and it also cannot detect more complicated implicit patterns that machine learning distinguishes. Besides, the rule-based approach frequently utilizes legacy solutions that are limited in processing capacity and speed.

Machine learning solutions, on the other hand, work by processing significantly larger sets of user and transaction data. This kind of software is capable of evaluating each transaction using more variables. Instead of checking the activity against each separate explicit rule, ML technology compares the pattern of the current transaction to previously recorded patterns, looking at the larger picture as opposed to examining isolated features. This helps catch more subtle interference, and it also allows the software to distinguish newer threats that haven’t been recorded before.

On top of that, machine learning in finance enables you to reduce the amount of the manual work needed to ensure sound security. Automation is one of the key advantages of ML.

Since ML systems get better with time, learning from previous experiences, they require drastically less continuous input from humans, and they’re capable of working autonomously in not only detecting fraud but taking appropriate measures to stop an attack, minimize damages, and provide a better experience by decreasing the number of verification steps.

Practical ML algorithms to combat fraud

Now that you understand the main advantages of ML for financial cybersecurity, you may be wondering how to use machine learning to detect fraud. ML engineers employ supervised and unsupervised learning algorithms to counter different types of fraud.

Let’s take a look at several of the most widely used techniques.

Supervised algorithms

A supervised algorithm is an example of how banks are using machine learning to minimize fraud when they have annotated datasets. Such a dataset is a collection of variables with known labels, meaning an ML model can use this dataset to learn fraud patterns.

The most common supervised learning algorithms that the financial services sector uses include

- Logistic regression

Logistic regression is a simple and quick-to-implement algorithm that predicts the probability of an event based on selected variables. It outputs a number between 0 and 1, signaling about the likelihood of a particular transaction being authentic or not. Financial institutions use logistic regression to combat phishing and credit card fraud.

- Decision trees

A decision tree is an algorithm that applies different rules to verify data at each step and splits the data accordingly.

In fraud prevention, decision trees are introduced to training sets that describe legitimate customer behavior inherent to your system, as well as occurrences of fraud, enabling the ML model to distinguish it.

- Random forest

This fraud detection algorithm builds upon the previous one, using a set of decision trees. Random forests output the average of the predictions of randomized decision trees, thus reducing the threat of overfitting—a case when a model becomes excessively tailored to its training datasets, making it ineffective for work with new information.

- Neural networks

Neural networks operate on the basis inspired by the functioning of the human brain. As a fraud detection model, a neural network can be incredibly effective in detecting and interpreting non-linear relationships between data points. They can be applied to a wide range of tasks, from identifying online hacking attempts to distinguishing a forged ID.

Unsupervised algorithms

In unsupervised learning, ML models don’t work with labeled data. They have to classify fraud instances by grouping data points within datasets by their similarity to each other and detecting abnormalities.

- K-means clustering

K-means is a clustering algorithm. It works on unfamiliar datasets by grouping data points that are near each other. After the first division, the algorithm evaluates the distribution of features and repeats it, improving the accuracy on each iteration, until it produces the final result. In terms of fraud prevention, k-means is an effective way to detect standalone points, thus finding abnormal and potentially malicious activities.

- One-class SVM

This model is useful for battling new types of financial fraud, as well as more typical scenarios. One-class SVM algorithm detects events that happen extremely rarely, in the context of the system it is applied to. It singles out cases that have little to no instances in a company’s databases and marks them as suspicious activity.

- Local Outlier Factor (LOF)

LOF is another classification algorithm applied in fraud detection software. It clusters data, similarly to k-means, and surveys the density of values at each location. The points with low density host too many values that are far from the others. These are considered to be “outliers,” and they may represent fraudulent activity attempts.

- Isolation forest

Fighting fraud using machine learning is effective with the isolation forest algorithm. This model relies on decision trees but, unlike random forest, it is unsupervised. Isolation forest follows different principles than most classification models.

Instead of creating valid profiles of points and pinning down abnormalities that don’t fit in, it works by looking for anomalies from the get-go. This reduces memory demand for this algorithm and enables higher processing speeds.

How to get started?

ML technology is rapidly gaining momentum as companies’ biggest asset in the fight against fraud. Financial fraud comes in many forms—from offline bank scams to identity theft, phishing, and money laundering schemes—all of them being damaging to both fintech businesses and their clients.

As far as tools for preventing financial fraud go, machine learning is among the most efficient, reliable, and flexible solutions. It improves the accuracy of fraud detection and removes a substantial part of the manual work required, reducing your company’s expenses while enhancing its security.

If you’re interested in incorporating fraud detection machine learning algorithms into your operations, Eastern Peak specialists will be delighted to help you begin this journey.

Book a free consultation with us to discuss how ML can protect your business.

Read also:

About the author:

Alexey Shalimov, CEO at Eastern Peak

As CEO at Eastern Peak, a professional software consulting and development company, Alexey ensures top quality and cost-effective services to clients from all over the world. Alexey is also a founder and technology evangelist at several technology companies. Previously, as a CEO of the Gett (GetTaxi) technology company, Alexey was in charge of developing the revolutionary Gett service from ground up and deploying the operation across the globe from New York to London and Tel Aviv.